May 18, 2001

News Flash: World Demand for Grain Increased During Years of Asian Crisis

When agricultural prices and incomes fall, analysts usually look to an external event for an explanation, or some might say, to blame. The event that continues to be mentioned for the current siege of depressed grain prices is a slump in world demand via the domino effect of the Asian Crisis beginning in late 1997. We continue to hear this explanation from both the Congressional and Executive Branches as well by officials of farm organizations and commodity groups.

There are two problems with this explanation. One is that the data don’t support it. World grain demand did not slump during the last years of the decade of the 1990s. It was a supply surge not a demand slump that put the grain markets in distress.

Secondly, the real problem is not that this or that event/disturbance occurred but that grain markets tend not to self-adjust like other industries. In the case of the grain markets, low prices do not render a timely cure for low prices. The production response is too small from the supply side and the quantity demanded response is too little from the demand side to sufficiently reduce inventories and to raise prices in a reasonable length of time. Readers of this column are familiar with the lack of adjustment argument.

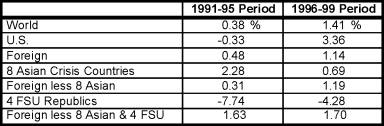

Since the “world demand slump” explanation continues to be offered up as “the” problem, let’s go the numbers. Table 1 shows average rates of growth in total grain domestic demand for several geographical delineations.

Table 1. Total Grains: A comparison of the rates of growth (%) in domestic demand between the 1991-1995 period and the 1996-1999 period. The eight Asian Crisis countries include Japan, South Korea, Taiwan, Hong Kong, Philippines, Malaysia, Indonesia and Thailand. The four Former Soviet Union (FSU) Republics include: Russia, Ukraine, Kazakstan and Uzbekistan. (Computed from USDA PS&D data)

The annual rate of growth of total grain demand for the eight Asian Crisis countries did decline during the 1996-99 period compared to 1991-95 (from 2.28% annually during 1991-95 to 0.69% annually during 1996-99). Incidentally, if soybeans are thrown in with total grains, the annual growth rate of domestic demand for grains and soybeans in the Asian Crisis countries exceeded 2% for both periods. But I digress.

The issue is: did the Asian financial crisis precipitate demand reductions in other parts of the world and thus cause worldwide grain demand to decline or “slump”? The tabled data suggest that the answer is no.

Foreign total grain demand, that is domestic grain demand in all countries except the U.S., grew at a faster rate during the 1996-99 period than during the “golden years” of 1991-95 (0.48% in 1991-95; 1.14% in 1996-99).

If the eight Asian Crisis countries are taken out of the “foreign” designation, the domestic demand for grains also grew faster during the 1996-99 period than during 1991-95 period. Notice that if the four former Soviet Union (FSU) countries and the eight Asian Crisis countries are taken out of foreign, the average annual rates of domestic demand for total grains are nearly identical for the two periods.

Since world, rather than foreign, demand is more often mentioned, how did world total grain domestic demand fare for the two periods? World total grain demand grew at an annual rate of 0.38% in the 1991-95 period and 1.14% the 1996-99 period. Clearly, world total grain domestic demand did NOT drop and therefore did not cause grain prices and market incomes to crash.

If a slowdown in demand is not the disturbance source, what about the supply side? Table 2 shows production annual rates of growth for the 1991-95 and 1996-99 periods for the world, foreign and the U.S. In all cases, the annual growth rates were higher for the latter of the two periods.

Table 2. Total Grains: A comparison of the rates of growth (%) in production between the 1991-1995 period and the 1996-1999 period. (Computed from USDA PS&D data)

It has been said that “if something is said often enough and long enough, it will be assumed to be true” whether it is or not. So, we must remember that it was a surge in world supply not a slump in world demand that knocked grain prices and incomes for a loop.

Of course, increases in worldwide supply can and usually does mean less export opportunities for U.S. There are two reasons for this. One is that production may have been larger among our export customers so they need to import less. Secondly, our export competitors may have experienced increased production as well, and, since they tend to carry minimal stocks from one year to the next, they capture a larger share of the export market. The U.S. on the other hand allows stocks to change rather than sweeping all the excess into the export market which tends to make us the residual supplier.

A slump in demand carries with it the expectation that demand conditions will improve. If the disequilibrium is caused by a permanent increase in supply rather than a short-term decrease in demand, the message is not as upbeat.

While many have declared that the financial crisis in Asia cascaded into a world demand problem, the data are clear. World demand for total grains increased during the time of the Asian Crisis. The problem is and was increased production in the U.S. and around the world.

Daryll E. Ray holds the Blasingame Chair of Excellence in Agricultural Policy, Institute of Agriculture, University of Tennessee, and is the Director of the UT’s Agricultural Policy Analysis Center. (865) 974-7407; Fax: (865) 974-7298; dray@utk.edu; http://www.agpolicy.org.

Reproduction Permission Granted with:

1) Full attribution to Daryll E. Ray and the Agricultural Policy Analysis Center, University of Tennessee, Knoxville, TN;

2) An email sent to hdschaffer@utk.edu indicating how often you intend on running Dr. Ray’s column and your total circulation. Also, please send one copy of the first issue with Dr. Ray’s column in it to Harwood Schaffer, Agricultural Policy Analysis Center, 310 Morgan Hall, Knoxville, TN 37996-4500.