June 15, 2001

Argentina’s Net Exports NOT South of Brazil(’s)

Brazil receives a lot of ink in the agricultural press, as well it should given the sharp expansion of Brazil’s soybean acreage and exports in recent years. But Argentina, Brazil’s neighbor to the south, deserves comparable attention. Averaged over the 1990s, Brazil and Argentina are neck-and-neck—or fender to fender in NASCAR lingo—in net exports of oilseeds, oilmeals and oils. When grains are lumped in with the oilseed complex, Argentina is the major-crop export powerhouse of South America and has been for decades.

In the case of net exports of oilseeds, oilmeals and oils, the two countries have come to within a hood ornament of one another from different starting blocks and at different rates of acceleration. Brazil’s oilseed acreage and exports took off in the 1970s and then settled back to more gradual but steady rate of expansion through the 1980s and 1990s. Argentina’s growth spurt in oilseed production and exports began later—in about 1980—but the high rate of growth has continued. By the early 1990s, Argentina’s net exports of the total of oilseeds, oilmeals and oils had caught up with Brazil. As the 20th century came to a close, Argentina consistently exported greater annual volumes of oilseeds, oilmeals and oils than Brazil. Since Argentina had less pent-up domestic demand for vegetable oil than Brazil, even more of the additional production in Argentina was channeled to the export market than in the case of Brazil. It is important to note that non-soybean oilseeds and products are included in the totals. About 20 percent of Argentina’s total oilseeds, oilmeal and oil would typically be from sunflowers while soybeans or soybean products would comprise nearly all of Brazil’s total.

Also, compared to Brazil, Argentina exports a greater share of total oilseeds and products in their processed form. On average during the 1990s, 82 percent of Argentina’s net exports of oilseeds, oilmeals and oils was in the form of oilmeal and other processed products. The comparable number for Brazil during this time was 65 percent. The U.S. percentage was 20 percent.

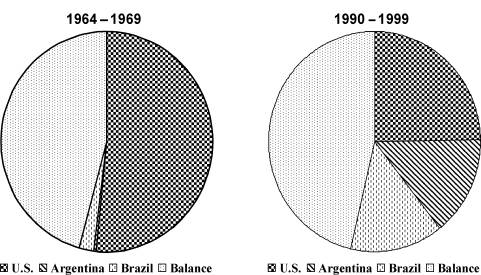

The growth in oilseed, oilmeal and oil exports by Brazil and Argentina has meant that their share of the world export market has gone from inconsequential in the 1960s to roughly 14 percent for Brazil and 15 percent for Argentina in the 1990s (see Figure 1). The U.S. share numbers are 52 percent in the 1960s and 25 percent in the 1990s. The collective share of the oilseed, oilmeal and oil world exports by exporting countries other than the U.S., Brazil and Argentina remained unchanged between the 1960s and 1990s at 46 percent.

Figure 1. A comparison of the share of the world oilseed, oilmeal and oil market held by the United States, Argentina, Brazil and the balance of the world between the 1964-69 period and the 1990-1999 period. Data source: USDA PS&D.

And there is more. Argentina is not only a net exporter of oilseed, oilmeal and oil, she also is a long-time net exporter of grains. Argentina annually exported over 8.8 million metric tons (mmt) of grain in 1960s and double that in the 1990s, most of which was wheat. In fact, because Brazil is a net importer of grains (again primarily wheat and primarily from Argentina), Argentina has a greater presence in the combined grain and oilseed export market than Brazil. In the 1990s, Brazil’s net exports of the total of grains (-7.9 mmt) and oilseed, oilmeal and oil (15.3 mmt) was 7.4 mmt while Argentina’s combined net exports (with grains represented 16.2 mmt) was 33.7 mmt. By comparison, the U.S. net exports of grains and oilseed, oilmeal and oil averaged 113.7 million metric tons during the 1990s.

Clearly, both Brazil and Argentina have come on like gangbusters in recent decades and continue to expand exportable surpluses without much regard for whether prices are “high” or “low.” When viewed over four decades and across grains as well as oilseeds, Argentina may be an even more imposing export competitor than Brazil.

Daryll E. Ray holds the Blasingame Chair of Excellence in Agricultural Policy, Institute of Agriculture, University of Tennessee, and is the Director of the UT’s Agricultural Policy Analysis Center. (865) 974-7407; Fax: (865) 974-7298; dray@utk.edu; http://www.agpolicy.org.

Reproduction Permission Granted with:

1) Full attribution to Daryll E. Ray and the Agricultural Policy Analysis Center, University of Tennessee, Knoxville, TN;

2) An email sent to hdschaffer@utk.edu indicating how often you intend on running Dr. Ray’s column and your total circulation. Also, please send one copy of the first issue with Dr. Ray’s column in it to Harwood Schaffer, Agricultural Policy Analysis Center, 310 Morgan Hall, Knoxville, TN 37996-4500.