US total planted acreage varies little despite wide swings in commodity prices

For as long as we can remember, we have made the point that farmers plant all their acres all the time. Recently, someone challenged us on that assertion using our favorite line, “Show me the data.”

To test our assertion, we chose a period that included low prices, high prices, declining prices, increasing prices, stable demand, and rapidly increasing demand. The time period we settled on was the era from 1998 through 2018. If farmers were going to increase major crop acres, the establishment of the renewable Fuels Standard which increased the demand for corn to be converted into ethanol should show a dramatic increase in crop acres. At the other end of the spectrum, if farmers were to reduce their acreage that should be apparent in the years after 2012 when farm income declined precipitously.

Let’s look at what we found.

During the 1998-2018 period, the season average price of corn varied from $1.82 (255.5 million planted acres for the eight major crops) in 1998 to $6.89 (257.4 million planted acres for the eight major crops) in 2012 (USDA-PS&D https://tinyurl.com/zwdoyyu for prices and USDA-NASS-Quick Stats https://tinyurl.com/yctmdk5z for acreage).

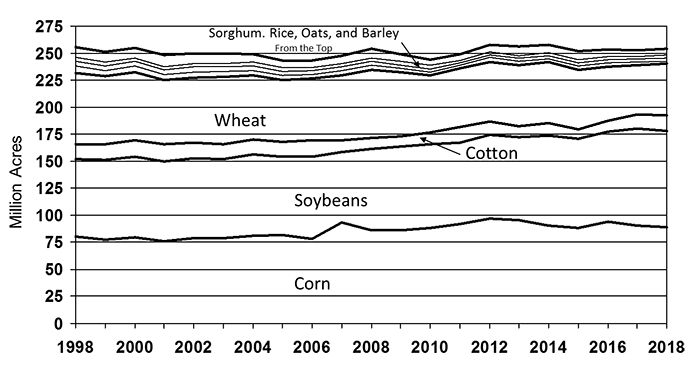

Figure 1. Stacked chart of area planted to the eight major crops in the US (corn, soybeans, cotton, wheat, barley, oats, rice, and grain sorghum), million acres, 1998-2018. (Source: USDA NASS, Quick Stats)

The 8-major-crop planted acreage ranged from 243.2 million acres in 2005 to 257.8 million acres in 2014 (Figure 1). The period started out with 255.5 million acres planted to the eight major crops in 1998 and ended with 254.2 million acres in 2018, a decline of 1.3 million acres.

In this same period corn and soybean planted acreage increased from 152.2 million acres to 178.8 million acres with 18 million of the 26.1-million-acre gain coming from wheat. Cotton gained 700 thousand acres and the remainder of the difference came out of barley, oats, rice, and grain sorghum.

With agriculture, there is an asymmetric response to changes in price. In response to lower prices, farmers do not reduce their production, in part because they don’t know what the price will be during the period when they will be marketing their crop. There is always the possibility that there will be a drought or other limited production somewhere else and if they do not plant, they won’t have anything to sell in that situation.

With relatively high fixed costs consisting of land and equipment and lower variable costs, farmers have every incentive to plant all their land in the face of low prices because any income above the variable cost of production goes toward covering fixed costs. In the short-run, crop farmers will produce even if the price does not cover variable costs in hopes of a price rally.

Farmers will plant whether the own the land or rent it. If they own it, there is little economic reason to leave it idle and if it is rented ground, it makes no sense to pay the rent and then not use the land. If the farmer cannot obtain the finances to put the crop in, the land will be snatched up by farmer with adequate financial resources to cover any losses that might be incurred in the short run. That also allows replacement farmers to spread their fixed costs out over more units of production, lowering the cost of production per unit of production.

On the other hand, with high prices farmers have an incentive to increase their planted acres. This did not happen in the US in this era in part because the most suitable acres to bring into production were under a 10-year contract in the Conservation Reserve Program, so only a small number of acres were available each year during the high-corn-demand period. Beyond that, there were few remaining acres that could easily be brought into production. The US has a mature agricultural economy with most acres allocated to their optimal use.

Brazil, on the other hand is in the situation where the US was in the 19th century with an expanding frontier and plenty of suitable acres that with some investment can be converted to agricultural production.

In addition, farmers are reluctant to give up rented ground in periods of low prices because they will not have access to that land when prices exceed the full cost of production. In the face of low prices, farmers may switch to a crop where their losses are lower, but in the short- to medium-run—farmers are always in the short to medium-run until the banker refuses to loan them the money to put in the next crop—they virtually plant all their cropland all of the time.

Whether it is in Brazil or the US, when it comes to annual planting decisions, farmers tend to plant all their cropland to one crop or another, as illustrated by the US 8-crop planted acreage numbers from 1998 to 2018.

Policy Pennings Column 996

Originally published in MidAmerica Farmer Grower, Vol. 37, No. 242, October 4, 2019

Dr. Harwood D. Schaffer: Adjunct Research Assistant Professor, Sociology Department, University of Tennessee and Director, Agricultural Policy Analysis Center. Dr. Daryll E. Ray: Emeritus Professor, Institute of Agriculture, University of Tennessee and Retired Director, Agricultural Policy Analysis Center.

Email: hdschaffer@utk.edu and dray@utk.edu; http://www.agpolicy.org.

Reproduction Permission Granted with: 1) Full attribution to Harwood D. Schaffer and Daryll E. Ray, Agricultural Policy Analysis Center, Knoxville, TN; 2) An email sent to hdschaffer@utk.edu indicating how often you intend on running the column and your total circulation. Also, please send one copy of the first issue with the column in it to Harwood Schaffer, Agricultural Policy Analysis Center, 1708 Capistrano Dr. Knoxville, TN 37922.