China’s dramatic growth in soybean imports and its commodity price impact

One of our readers raised a question about a statement we included in a recent column on China’s impact on world agricultural commodity prices. In the column titled “USDA top officials versus USDA data” we wrote, “In the current environment, China’s increase in demand for oilseed complex needs to be put in context. Rather than placing a significant upward pressure on world crop prices over the last decade, it could be argued that China’s increase in soybean imports for use as animal feed has lit a bonfire fire under the feet of Brazil’s agricultural sector” http://agpolicy.org/weekcol/409.html. Let’s take a look at China and world soybean markets over the last 17 years.

In contrast to other major crops, over the last decade China has become dependent on imports to meet its domestic soybean needs. Prior to that time, China was nearly self-sufficient in soybean production.

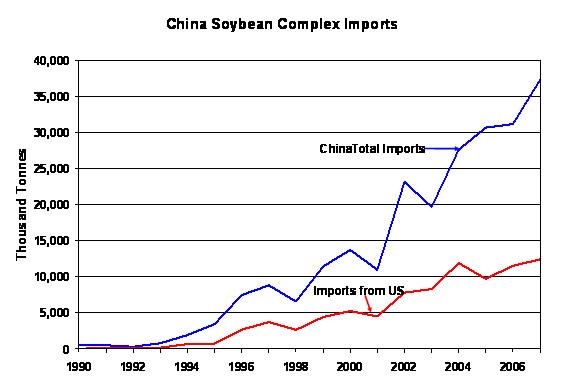

Between 1971 and 1993, China’s imports of soybean complex (soybeans, soybean meal and soybean oil) ranged from 0 to 910 thousand tonnes. Then, China’s imports began to explode increasing from 1.9 million tonnes in 1994 to 37.3 million tonnes in 2007.

Figure 1. China Soybean Complex Imports, total and imports from the US, 1990-2001.

Source: USDA PS&D (http://www.fas.usda.gov/psdonline/).

China moved from being a small player in world soybean markets to accounting for 26 percent of the world soybean complex export market. During the same time, China’s soybean complex imports from the US increased from 665 thousand tonnes in 1994 to 12.4 million tonnes in 2007 accounting for one-third of all of China’s soybean complex imports.

Over the last five years, 91 percent of China’s soybean complex imports have been soybeans with most of the balance soybean oil. All of the imports from the US have been soybeans.

Looking at those numbers, it is clear that China has become an important soybean customer for US exports. But except for brief periods like the last two years, that growth has been accompanied by unremarkable $4.50-$5.50-like soybean prices. So there must be other things going on. Yes, it is important to look at the supply side.

Before looking at world side-supply considerations, there is one thing on the US demand side that is of passing interest.

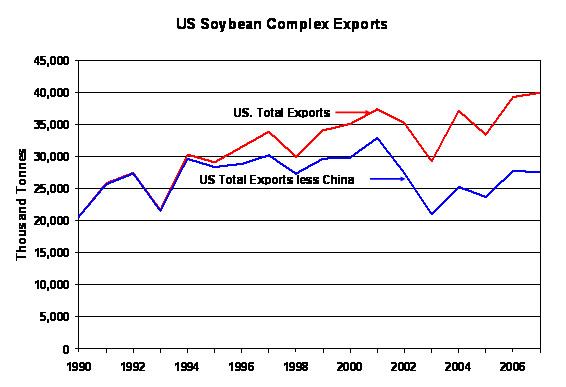

While China accounts for 31 percent of US soybean exports, some of the soybean exports to other countries have been lost to competitors.

Between 1994 and 2003, US soybean complex exports increased from 30.3 million tonnes (Fig. 2) to 40 million tonnes, and increase of 9.7 million tonnes. At the same time US complex exports to countries other than China declined from 29.6 million tonnes to 27.9 million tonnes, a drop of 2 million tonnes.

Figure 2. US Soybean Complex Exports, total and total less China, 1990-2001.

Source: USDA PS&D (http://www.fas.usda.gov/psdonline/).

But it is the supply side of the market that has to be looked at to see why much of China’s remarkable increase in imports occurred when soybean prices were in the doldrums.

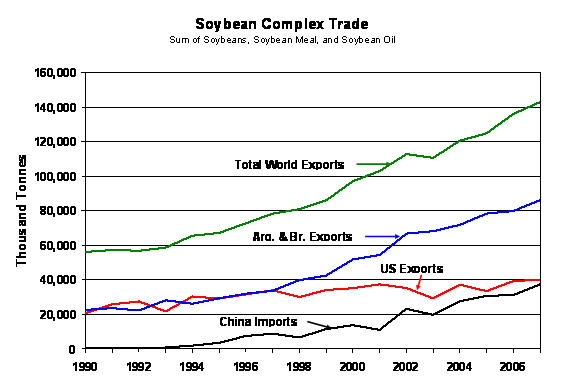

While China became an important soybean import customer, the US did not maintain its once dominant share of the total soybean export market. During the 1994-2007 period in which US total soybean complex exports increased by 9.7 million tonnes, world exports of soybean complex increased by 77.5 million tonnes (Fig. 3).

The US captured 13 percent of 77.5 million tonne increase with the giant share of the balance going to Argentina and Brazil. As Figure 3 shows, China’s soybean complex imports comes closer to running parallel to the exports of Argentina and Brazil than it does the US.

Figure 3 Soybean Complex Trade, total world exports, Argentina and Brazil combined exports, US exports and China imports, 1990-2001. Source: USDA PS&D (http://www.fas.usda.gov/psdonline/).

It is indeed the world supply side that holds the explanation of why soybeans prices followed, not lead, the early portion of recent increases in grain prices and did not provide prosperous soybean prices during late 90s and early 2000s when Chinese imports were sky rocketing.

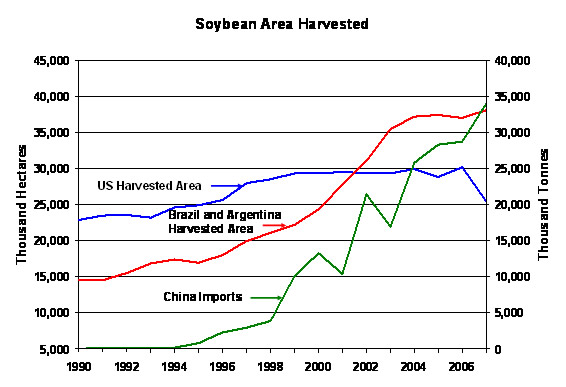

Figure 4 shows total soybean acreage increase in Argentina and Brazil with China’s imports of soybean complex (Fig. 4). Since the mid-1990s, with the exception of 2007, US harvested soybean area has been up slightly while the area in Brazil and Argentina has doubled.

Figure 4. Soybean Area Harvested Compared to China Imports,

Us harvested area, Brazil and Argentina combined harvested area and

China soybean complex imports, 1990-2001.

Source: USDA PS&D (http://www.fas.usda.gov/psdonline/).

It seems clear to us that the major beneficiaries of soybean complex imports by China and the rest of the world over the last 17 years have been the soybean producers and Brazil and Argentina. The US share of the increase pales by comparison.

In pointing that out, it must be recognized that most of the productive cropland in the US is in use, while Brazil has the potential to bring millions of additional acres into production. Given its relatively fixed land base, the US alone could not have met the increased demand for soybeans and still planted any significant amount of corn and wheat.

Of course, much of the recent run-up in soybean prices was not because of an above trend demand for soybean-complex products but because corn competed for millions of US acres that otherwise would have been in soybeans.

Soybean prices were nothing to write home about during most of the last decade. But China’s dramatic and steady growth in soybean imports benefited US farmers in the1998-2001 period by keeping soybean prices from tanking as badly as corn prices.

Daryll E. Ray holds the Blasingame Chair of Excellence in Agricultural Policy, Institute of Agriculture, University of Tennessee, and is the Director of UT’s Agricultural Policy Analysis Center (APAC). (865) 974-7407; Fax: (865) 974-7298; dray@utk.edu; http://www.agpolicy.org. Daryll Ray’s column is written with the research and assistance of Harwood D. Schaffer, Research Associate with APAC.

Reproduction Permission Granted with:

1) Full attribution to Daryll E. Ray and the Agricultural Policy Analysis Center, University of Tennessee, Knoxville, TN;

2) An email sent to hdschaffer@utk.edu indicating how often you intend on running Dr. Ray’s column and your total circulation. Also, please send one copy of the first issue with Dr. Ray’s column in it to Harwood Schaffer, Agricultural Policy Analysis Center, 309 Morgan Hall, Knoxville, TN 37996-4519.